A Greek Hit +4 Sigma and Meant Nothing: Measuring Options Repositioning

A BTC Vomma z-score held above +4 sigma for eight hours and looked like a volatility-convexity regime change. Ninety-eight percent of it was spot walking away from the strikes. Here is why a Greek z-score is not a position, and the maths of an OI-weighted repositioning measure that is.

Z-score normalization is one of the cleaner ideas in a Greek dashboard. Take every Greek, compare its current value against its own rolling history, and colour the cell by how many standard deviations it sits from its recent mean. Do it across all 37 Greeks and four derivative orders and you get a single surface that answers a precise question at a glance. Which Greek, right now, is furthest from its own normal.

That question is legitimate and the method is sound. The heatmap below is a good anomaly detector. This note is about what the answer to that question does, and does not, tell you about positioning, and it ends with the maths of a measure built to answer positioning directly.

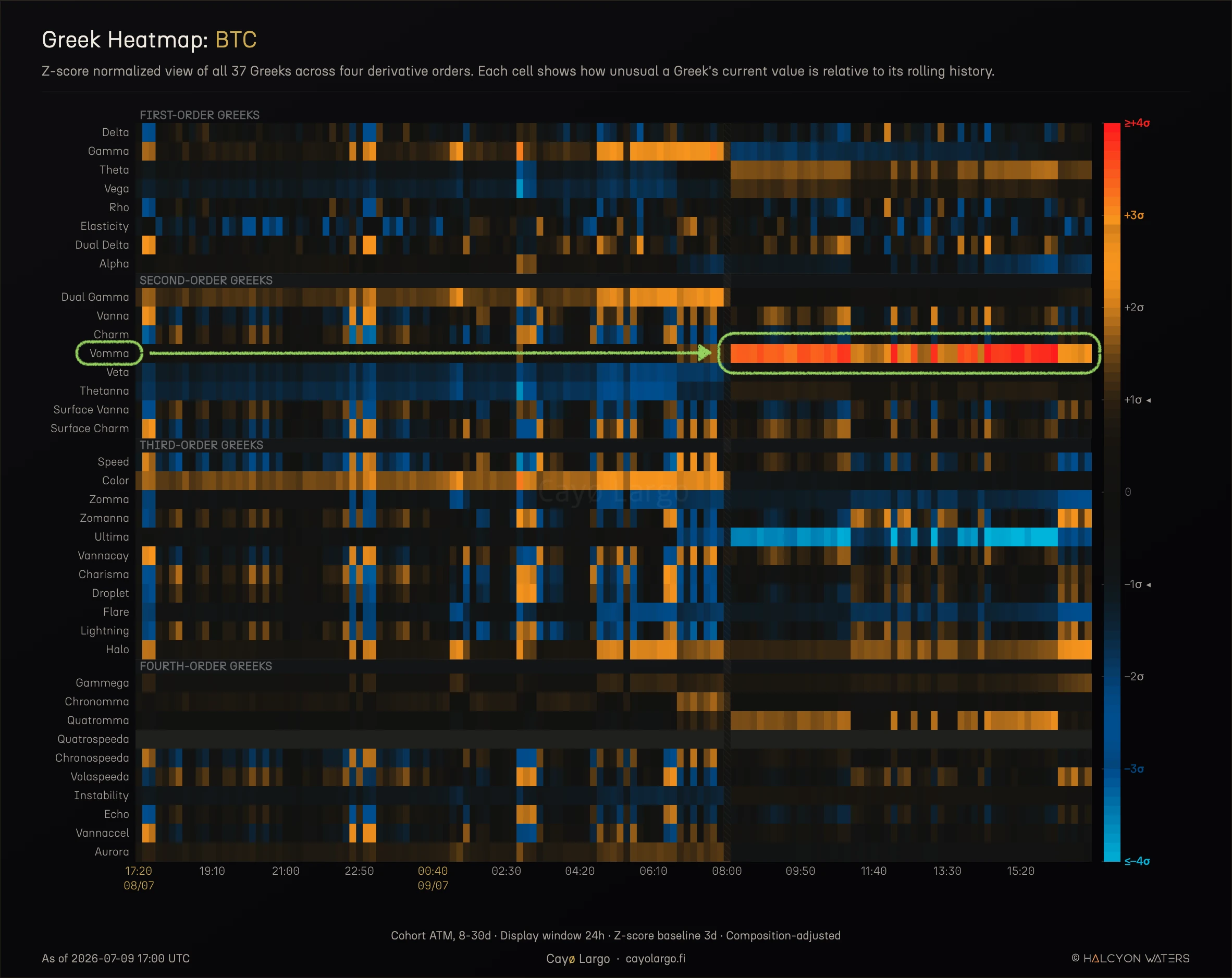

Figure 1: BTC Greek z-score heatmap, all 37 Greeks by derivative order, ATM 8-30d, over 24 hours. Warm is above the rolling mean, cool is below. Most rows flicker as spot and vol move. One row does not, and the marker points to it. The Vomma band locks solid red from roughly 07:40 UTC and holds above four standard deviations for eight hours. We follow the green thread through all three figures.

A Row That Would Not Cool Down

Read Figure 1 and your eye goes straight to the Vomma row in the second-order block. Every other Greek breathes, warm then cool, as the market moves through the day. Vomma pins itself at the top of the scale and stays there. Composition-adjusted, against a trailing three-day baseline, it steps from about zero to above three near 07:40 UTC on 09 July and peaks close to +4.2.

Four sigma is a one-in-fifteen-thousand event under a normal. On a second-order vol Greek that reads as a convexity regime change, someone loading up on exposure to large moves in volatility. Drill into the single-Greek strip and the story looks even stronger.

Figure 2: The Vomma drill-down. The marker sits on the plateau, the z-score in red holding above three for eight hours and touching four. The raw value in grey whipsaws between 150 and 450. The market-context panel below shows what actually happened over the same window, spot walking up through the strike ladder while ATM implied vol drifts a couple of points lower. The z-score is tracking the price panel, not a trade.

The market-context panel underneath is the tell. Across the eight hours the z-score is elevated, spot is climbing and implied vol is falling. If this were a convexity bet you would expect it to show up as demand, a bid for vol-of-vol, not as a quiet drift in the opposite direction. So we fixed the instrument set and decomposed the move. Ninety-seven point eight percent of it came from spot walking away from the strike ladder. One tenth of one percent came from the 2.6 vol-point change in implied vol. There was no Vomma bet. The heatmap was doing exactly what it is built to do, and the honest reading of its output is not the one the colour invites.

What a Z-Score Can and Cannot Tell You

Start from the definition. For a Greek with a rolling mean and rolling standard deviation the cell is

This is a well-posed question whenever the baseline distribution of has a location and a spread. It asks how far today's value sits from its typical value, in units of its typical variation. Nothing about that is unsound.

The constraint is upstream of the z-score, in what is. A Black-Scholes Greek is a deterministic function of four inputs, spot , strike , time to expiry and implied vol . Aggregate a set of Greeks with fixed weights over a fixed set of options and the aggregate is still a deterministic function of those same inputs. Trading is not one of the inputs. So a z-score built on such an aggregate can move for exactly three reasons, spot moved, the clock ran, or the surface moved. It has no channel through which a trade can enter.

That is the whole of it. The Greek z-score heatmap is a market-state anomaly detector. It answers, is the current state of spot, time and vol unusual for this Greek. When the answer is yes it colours a cell, and the cell is telling the truth. It is simply not the truth most readers project onto it, which is that someone did something. A number can look like a signal and be drift, a cousin of the way IV momentum on a thin strike looks violent while nothing reprices.

Why At-the-Money Vomma Sits on a Vertex

Vomma is the reason this particular row screamed, and the reason is structural. Vomma is the sensitivity of vega to implied vol, , and it carries a clean identity against vega,

We checked this on live data and it returned one point zero zero zero zero zero zero on every row, calls and puts alike, as put-call parity requires. Now write the two moneyness terms with ,

and multiply them out,

The product is a parabola in . At the money, where , it sits at the bottom of that parabola, , a small negative number near the vertex. So an at-the-money cohort has a Vomma-over-vega baseline pinned near a minimum, and its rolling mean is close to zero. That is a degenerate location. A z-score with a near-zero baseline and a small denominator will fly the moment moves off zero, because the term grows quadratically while the baseline had almost no location to begin with.

This is not special to Vomma. We ran the whole Greek set through a stability screen in the at-the-money cohort, and 11 of the 19 Greeks predicted to be degenerate came back with no location at all. The genuinely valid Greeks sat well clear of them, with a clean empty gap in between. The decisive test was the wings. Move the same Greeks into the below-spot cohort, away from the vertex, and they recover a location almost across the board. Vanna, charm, surface charm, Vomma, all find a footing off the money. A Greek can be degenerate at the money and perfectly readable in the wings, which is why any honest gate on this surface has to be computed per Greek and per cohort, not once for the whole grid.

One corollary is worth stating plainly, because it catches people. You cannot use one Black-Scholes Greek to confirm another. They share and , so their ratios are algebraic identities. In our data the correlation between Vomma-over-vega and ultima-over-vega was minus 0.997 before the move and minus 0.9997 after. That is not two signals agreeing. It is one deterministic function printed twice.

The Composition Trap

There is a second way this surface misleads, and it has nothing to do with the market moving. It is the cohort changing shape underneath the average.

The heatmap plots a weighted average over a cohort, and the cohort's membership is not fixed. Options age in and out of the 8-30 day band, strikes drift across the moneyness boundary, and the option count jumps between discrete regimes. In the at-the-money BTC cohort we studied it was bimodal, sitting at 8 members on some bars and 12 on others, with an 18-member regime earlier in the window. When the membership flips, the average reshuffles even if not a single option repriced, because the off-money members that carry most of the Vomma enter or leave the basket.

The damage is quantitative. We regressed the liquidity-weighted average Vomma on spot, time and vol and got an of only 0.36, when the deterministic argument says a fixed-composition aggregate should be near one. The missing variance was not positioning. It was composition. The average correlated with the raw option count at 0.70. Condition on a fixed membership, the 8-member bars alone or the 12-member bars alone, and the jumps back to about 0.95, exactly the mechanical determinism the theory predicts. Pooled across a changing cohort, that determinism is buried under membership noise, and a pooled standard deviation built on that noise is a meaningless denominator for a z-score.

So the at-the-money Vomma z-score has two independent problems stacked on top of each other. Its numerator is lifted by spot leaving a degenerate vertex, and its denominator is inflated by a cohort that keeps changing its members. Neither problem is a bug in the code. Both are what you get when you put a z-score on a deterministic quantity measured over a churning basket.

Splitting the Move Into Revaluation and Trades

If the z-score conflates market drift and trading, the fix is to stop averaging the Greek and start measuring exposure, then split its change into the part that is drift and the part that is trading. Both fall out of one product rule.

Define the exposure of a cohort in Greek as the open-interest-weighted, signed sum over its member strikes,

where is the open interest at strike and is a sign we return to below. Now take the change between two ten-minute snapshots. For a strike present in both, expand the difference of the product,

with and . Sum over the cohort and the change in exposure splits into three named channels,

Read the channels. The market channel holds open interest fixed and lets the Greek move. It is the book being revalued because spot and vol changed, with no trade behind it. This is precisely the deterministic quantity the z-score was picking up, now isolated in its own term. The repositioning channel holds the Greek fixed at its current value and lets open interest move. It is the exposure added or removed by actual trading on strikes that stayed in the cohort. The membership channel, , collects strikes that entered or left the cohort between the two bars, the calendar effect that wrecked the average. The three sum exactly to the change in exposure, so nothing is double-counted and nothing is thrown away.

Applied to the Vomma episode, the arithmetic matches the postmortem. Almost the entire move lands in the market channel. The repositioning channel is quiet. The heatmap saw a four-sigma anomaly because it could only see the sum, and the sum was dominated by the one term that carries no information about trading.

Weighting by Position, Not by Liquidity

Two weighting choices separate the exposure measure from the heatmap, and both matter.

The heatmap weights each option by a liquidity score. That is the right weight for a different question, how much to trust a given quote. It is the wrong weight for positioning, because a deep, liquid at-the-money option and a thin, illiquid wing option can carry very different amounts of open interest, and it is the open interest, the standing size, that a position is made of. Open-interest weighting answers the size question directly.

Does it actually add information beyond the deterministic core. We tested it on a fixed strike set, the case where the market channel is mechanical by construction. The liquidity-weighted average came back at around 0.95, deterministic as expected. The open-interest-signed exposure kept about 35 percent of its variance independent of spot, time and vol, even with membership held fixed. That residual is the thing the whole exercise exists to surface. It is positioning, and it is invisible to any measure that only sees the level.

The prerequisite is that open interest moves intraday, and it does. Across the cohort the fraction of ten-minute bars on which a strike's open interest changed ran at 0.051, more than seven times the 0.0069 you would see if open interest were a once-a-day snapshot. The repositioning channel is not forced to be a daily object. It has genuine ten-minute dynamics to measure.

The sign is the last choice, and it comes in two conventions.

| • | Net. Calls count plus one and puts minus one, the textbook call-minus-put convention. It assumes long calls and short puts and takes no view on who is on which side. |

| • | Dealer. Each strike is signed from live Deribit taker flow, so the sign reflects the market-maker side actually observed rather than an assumption, and it falls back to the net convention where flow is thin. On a reconciliation test the dealer-signed gamma matched the independent GEX pipeline to correlation one, which is the check that the sign is not inventing structure. |

The Repositioning Channel and Its Colour

Pull the repositioning term out on its own and it is the measure we wanted from the start,

The sum runs only over continuing strikes, those in the cohort at both bars, so membership never enters. Only the change in open interest counts, so revaluation never enters. What is left is trading, signed and open-interest-weighted. It is silent when nobody repositioned, which is the opposite of a z-score that is loudest exactly when the market is quietest and drifting.

The sign convention is the case function from above,

Repositioning is additive across time, so a ten-minute channel sums cleanly to any coarser bar. For an hourly display we sum the six ten-minute values, then map the result to colour against a fixed percentile scale so a busy hour reads bright and a normal one reads dark,

The scale is the 95th percentile of the absolute repositioning over a 30-day baseline, one yardstick for what a large move is in this Greek. A z-score would divide by a standard deviation, which the composition problem showed can be an inflated and meaningless number on a churning cohort. The 95th percentile of the magnitude survives a distribution that is zero most of the time, which is exactly what a genuine flow series looks like.

Colour it and the surface reads the way the eye expects. Blue where exposure was added, orange where it was removed, brightness scaled to the size of the trade against a normal month, dark where nothing happened. Point it at the same book and the same week, and the anomaly answers itself.

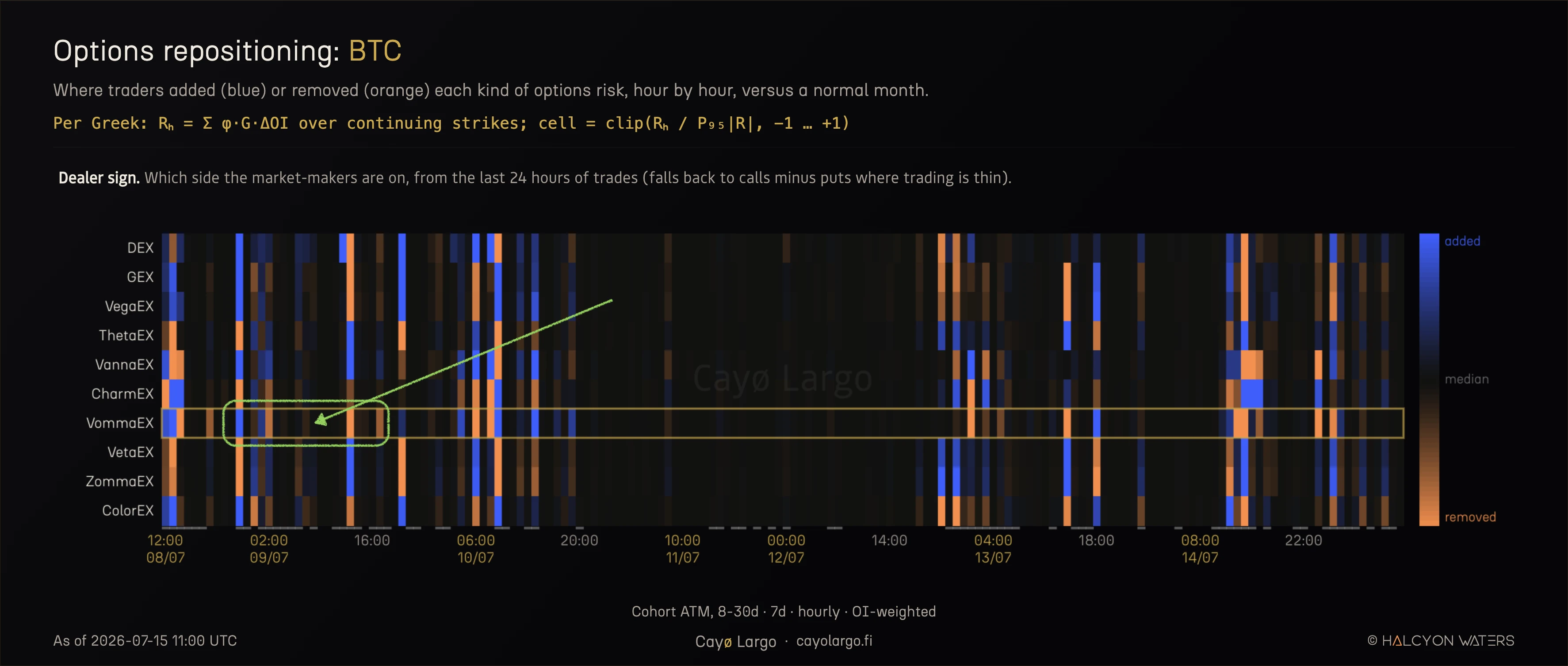

Figure 3: The same BTC book, read as repositioning, over the week that holds the anomaly. Ten OI-weighted exposures by hour, dealer sign, with the VommaEX row highlighted. Blue is exposure added, orange removed, brightness by the size of the move against a 30-day normal. The green thread lands here, on 09 July, the morning and afternoon Figure 2 held above four sigma. The VommaEX row there is dark. No repositioning ran while the z-score screamed, because there was no Vomma trade to run it. The bright VommaEX cells elsewhere in the week are the hours the desk did move that risk, and they look nothing like the flat stretch on the 9th.

What Each View Sees, and What It Misses

Neither view replaces the other. They answer different questions, and the honest move is to keep both and read them for what each does well.

| • | The z-score heatmap is strong at anomaly detection. It scans all 37 Greeks at once and flags the moment any one of them leaves its recent history. When you want to know that the surface has entered an unusual state, and which order of Greek feels it first, it is the right instrument, and it needs no open-interest data to work. |

| • | The z-score heatmap is weak as a positioning read. Its quantity is deterministic in spot, time and vol, so it fires on market drift rather than trading. It degenerates at the money where a Greek sits on a vertex, and its denominator inflates when the cohort churns. A bright cell is a true statement about market state and a poor proxy for what anyone did. |

| • | Repositioning is strong at isolating trading. It measures the open-interest change on continuing strikes, so revaluation and calendar rolls are removed by construction. It is silent when nothing traded, it survives the vertex and the composition trap that break the average, and it carries a dealer sign checked against an independent pipeline. |

| • | Repositioning has its own limits. It needs open interest at a real intraday cadence, it reports the change and not the standing level, an hourly display averages over sub-hour detail, and the dealer sign is an estimate from taker flow rather than a settled fact. It tells you where the desk moved, not where the desk sits. |

The Vomma row that would not cool down was not a mistake in the data or the maths. It was a correct answer to the question a z-score asks, read as an answer to a question it cannot ask. Spot walked away from the strikes and lifted a degenerate baseline, and the colour scale did the rest. Once you write the change in exposure as revaluation plus repositioning plus membership, the confusion resolves into arithmetic. The part that lit the heatmap sits in the market channel, and the part a trader wants sits in the repositioning channel, where the z-score never was. Figure 3 makes the same point without a formula. Hold the VommaEX row against the eight hours that lit the heatmap and it is flat, no trade to see.

The repositioning view runs live across coins and cohorts. For the standing level of exposure by strike, and how it decays into expiry, the surface view is the companion piece. For the price levels where dealer hedging flips, the Greek exposure projection is the third lens. Level, flow and hedge response, three readings of the same book, each honest about what it measures. The wider point, that knowing your Greeks is not the same as knowing the positioning behind them, we take up separately.

Frequently Asked Questions

Does a high Greek z-score mean a large position was put on?

Not on its own. A Black-Scholes Greek is a deterministic function of spot, strike, time and implied vol. Aggregate it over a fixed set of options and the aggregate is still deterministic in those inputs. A z-score on such a quantity can only tell you that spot moved, time passed, or the surface moved. It cannot see trading, because trading is not one of its inputs. To read positioning you have to measure the change in open interest, not the change in the Greek.

Why did BTC Vomma read +4 sigma without a Vomma trade behind it?

At the money, Vomma sits on the vertex of its own parabola in moneyness, so its baseline mean is close to zero and its z-score denominator is small. When spot walks away from the strike ladder the moneyness term grows fast and the ratio jumps. In the case we decompose, 97.8 percent of the move came from spot leaving the strikes and 0.1 percent from a 2.6 vol-point IV change. The z-score was measuring a small, degenerate baseline being lifted by price, not a convexity bet.

What is options repositioning and how is it computed?

Repositioning is the part of the change in a cohort's Greek exposure that comes from open-interest changes on strikes present in both snapshots, weighted by open interest. It is the sum over continuing strikes of the sign times the current Greek times the change in open interest. It excludes revaluation, the exposure moving because spot and vol moved with no trade, and it excludes membership, options ageing into or out of the cohort.

Is the z-score Greek heatmap useless then?

No. Z-score normalization across the Greek set is a sound way to flag temporal anomalies, moments when a Greek's value is far from its own recent history. That is a legitimate and useful question. The point is narrower. The answer to that question is dominated by market state, not by trading, so the heatmap is a market-state anomaly detector rather than a positioning tool. The two answer different questions and are best read side by side.

Why weight by open interest instead of by liquidity?

Liquidity weighting answers a data-quality question, how much to trust each quote. Open-interest weighting answers a positioning question, how much size sits behind each strike. To measure what the book carries and what changed in it, open interest is the correct weight. On a fixed strike set the OI-signed exposure keeps about 35 percent of its variance independent of spot, time and vol, and that residual is the positioning signal.

What is the difference between the net and dealer sign?

Net counts calls as plus one and puts as minus one, the textbook call-minus-put convention. Dealer signs each strike from live Deribit taker flow, so it reflects the market-maker side actually observed rather than an assumption, and falls back to the net convention where flow is thin. On the reconciliation test the dealer-signed gamma matched the GEX pipeline to correlation one.

Can you use one Greek to confirm another?

No. Second and higher Greeks share the same d1 and d2 building blocks, so ratios between them are algebraic identities. In our data the correlation between Vomma-over-vega and ultima-over-vega was minus 0.997, which is not evidence of anything. It is the same deterministic function seen twice. Confirmation has to come from open interest and trades, not from a second deterministic Greek.

Related Articles

Dealer Exposure Heatmaps for Crypto: Charm, Gamma and Vanna

Dealer Greek exposure heatmaps look simple and aren't. The full build for crypto options on Deribit: the charm, gamma and vanna maths and the order-flow sign.

Why Knowing Your Greeks Won't Save You on Deribit

You learned Delta, Gamma, Theta. You can explain Black-Scholes over coffee. Then you open Deribit's options page and none of it helps. Here's why options theory breaks down on a live screen.

Why Deep-OTM IV Momentum Is Noise, Not Signal

A stable IV smile but wild IV momentum at deep-OTM strikes. Why thin-strike microstructure is noise, not repricing, shown live on Deribit multi-coin data.